Introduction

Most real estate investors pour enormous energy into finding the next deal, negotiating terms, and managing tenants, but treat bookkeeping as a tedious afterthought. Without accurate, organized financial records, investors struggle to defend deductions during tax season, qualify for lender financing, and assess which properties are truly profitable versus cash-draining liabilities.

According to IRS Publication 527, rental property investors must "list your total income, expenses, and depreciation for each rental property" on Schedule E, a level of detail that requires systematic tracking from day one. Poor bookkeeping doesn't just mean frustration at tax time; it means missed depreciation deductions worth thousands annually, lost financing opportunities, and potentially serious audit exposure.

The good news: the right system prevents all of it. This guide is for rental property owners, house flippers, and portfolio investors ready to build financial systems that scale with their investments. Here's what you'll walk away with:

- A clear picture of what makes real estate bookkeeping uniquely complex

- Step-by-step guidance on setting up a compliant tracking system

- The key tax deductions to capture - and how to document them properly

- The most common (and costly) mistakes investors make, and how to avoid them

Key Takeaways

- Real estate bookkeeping tracks all financial transactions tied to your properties, the foundation for accurate taxes, smart decisions, and lender-ready records

- Real estate bookkeeping differs from general bookkeeping: it requires depreciation schedules, per-property tracking, and 1099 compliance

- Core components: per-property income tracking, operating vs. capital expense categorization, depreciation schedules, and monthly reconciliation

- Common mistakes include mixing personal and business finances, misclassifying capital expenses, and waiting until tax season to set up your books

- Set up a structured system early with professional support to scale your portfolio without losing financial visibility

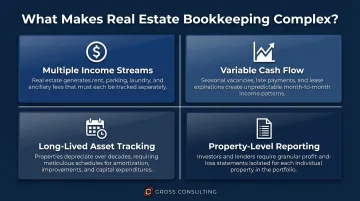

What Is Real Estate Bookkeeping and What Makes It Unique

Real estate bookkeeping is the systematic recording, organizing, and tracking of all financial transactions tied to investment properties, rental income, operating expenses, mortgage payments, capital improvements, and depreciation. Unlike general small business bookkeeping, real estate demands property-level granularity, multi-decade asset tracking, and compliance with specialized IRS rules.

Unique financial characteristics that increase complexity:

- Multiple income streams per property: Rent, late fees, lease penalties, application fees, and pet deposits each require separate tracking

- Highly variable cash flow: Large annual insurance premiums, property tax bills, and unexpected repair costs create uneven monthly cash flow even in profitable portfolios

- Long-lived asset tracking: Residential rental properties depreciate over 27.5 years under IRS Publication 946, requiring accurate basis records and depreciation schedules from acquisition forward

- Property-level reporting requirements: Per IRS Publication 527, Schedule E requires investors to report total income, expenses, and depreciation separately for each property, not just aggregate portfolio numbers

Regulatory obligations specific to real estate:

Real estate investors face compliance layers absent in most industries:

- Security deposits must be tracked as liabilities until retained, not recognized as income when received

- Form 1099-NEC must be filed for any contractor or vendor paid $600 or more annually

- 1031 exchanges require meticulous basis records and filing of Form 8824

- Syndications and joint ventures require tracking partner contributions and distributions separately

Cash vs. accrual accounting methods:

Per IRS Publication 538, most individual investors can use the cash method, income and expenses recorded when money changes hands. This method is simpler and works well for smaller portfolios. The accrual method, recording income when earned and expenses when incurred, provides a more accurate financial picture and is preferred by lenders. It's required only for C corporations and certain partnerships exceeding $31 million in average annual gross receipts.

Most landlords operating under individual or pass-through entity structures, LLCs taxed as partnerships or S corporations, qualify for cash-basis accounting. There's one important exception: even cash-basis investors must recognize advance rent as income immediately upon receipt, regardless of the period it covers.

Core Components of Real Estate Bookkeeping

Income Tracking

All rental income must be recorded per property and per tenant, distinguishing between:

- Standard monthly rent

- Late fees and lease penalties

- Application fees and pet deposits

- Refunds or credits issued

Use class tracking in QuickBooks or property tags in dedicated software to enable property-level profit-and-loss reporting. This granularity is essential for performance analysis, tax filing, and identifying underperforming assets.

Expense Categorization: Operating vs. Capital

The most tax-costly error investors make is misclassifying capital expenditures as operating expenses.

Operating expenses (deductible immediately):

- Repairs and maintenance

- Utilities, insurance, HOA fees

- Property management fees

- Professional services (legal, accounting)

Capital expenditures (must be capitalized and depreciated):

- Roof replacements

- HVAC systems

- Major renovations or additions

Per IRS Tangible Property Regulations, the IRS applies the BAR test (Betterment, Adaptation, Restoration) to determine whether an expenditure must be capitalized.

The de minimis safe harbor offers a practical workaround: investors without an applicable financial statement can expense items up to $2,500 per invoice rather than capitalizing them, provided the election is properly documented.

Depreciation and Asset Tracking

Depreciation is one of real estate's most powerful tax benefits. IRS Publication 946 confirms residential rental property depreciates over 27.5 years (commercial over 39 years). This deduction reduces taxable income even as the property appreciates in value, with no cash outflow required.

Critical requirement: Maintain accurate asset basis from acquisition. Land cannot be depreciated; investors must allocate purchase price between land and building. Failure to do so overstates depreciation and invites audit scrutiny.

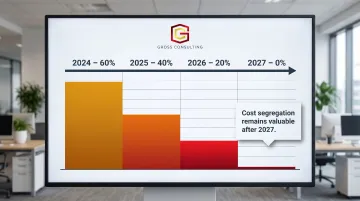

Cost segregation studies accelerate depreciation by reclassifying building components (appliances, carpeting, land improvements) into shorter-lived asset classes (5, 7, or 15 years). Bonus depreciation is phasing out - 60% in 2024, 40% in 2025, 20% in 2026, and 0% in 2027 per The Tax Adviser.

Investors with properties acquired in the last several years should consult a cost segregation specialist now to capture remaining bonus depreciation before the window closes.

Cash Flow Monitoring

Real estate cash flow is inherently uneven. Large annual payments for property taxes or insurance, unexpected repair costs, and tenant vacancies can make a profitable portfolio appear cash-poor in a given month.

Essential tools for avoiding surprises:

- Monthly cash flow statements

- Reserve fund tracking for capital replacements

- Variance analysis comparing actual vs. budgeted expenses

Without these, investors risk depleting reserves during vacancy periods or deferring essential maintenance.

Reconciliation

Reconciliation verifies that all transactions in your accounting system match corresponding bank, mortgage, and property management statements. Monthly reconciliation catches errors like:

- Uncredited escrow refunds

- Misclassified loan principal vs. interest payments

- Missing rent deposits

- Duplicate vendor payments

Skipping reconciliation creates compounding inaccuracies that are costly to unwind. By the time tax season or a lender due diligence request arrives, books that haven't been reconciled regularly require hours of reconstruction, and sometimes a professional to sort out.

How to Set Up Your Real Estate Bookkeeping System

Step 1 - Separate Finances

Open dedicated bank accounts and credit cards for each property or entity. Keep investment activity completely separate from personal finances.

Why this matters:

- Mixing personal and business funds creates tax preparation nightmares

- Makes it nearly impossible to document deductions defensibly

- Can undermine legal protections offered by LLC structures

Even if you operate a single rental property, a separate checking account is non-negotiable.

Step 2 - Build a Chart of Accounts

A chart of accounts is the financial blueprint of your bookkeeping system, organizing all income, expense, asset, liability, and equity categories.

Essential categories for real estate investors:

Income:

- Rental Income

- Late Fees

- Application Fees

Operating Expenses:

- Repairs and Maintenance

- Property Management Fees

- Insurance

- Property Taxes

- Utilities

- HOA Fees

Assets:

- Rental Property (Building)

- Land

- Capital Improvements

- Security Deposits Held

Liabilities:

- Mortgage Payable

- Security Deposits Payable

Equity:

- Owner Contributions

- Owner Distributions

This structure enables property-level tracking and supports accurate Schedule E reporting.

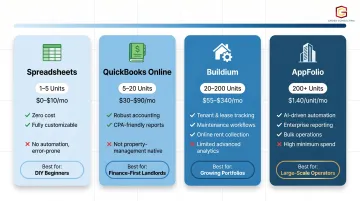

Step 3 - Choose the Right Software

Spreadsheets:

- Best for: 1-2 properties

- Limitations: Error-prone, no automation, difficult to scale

QuickBooks Online ($35-$235/month):

- Best for: 1-20 properties with CPA support

- Strengths: Class tracking, bank feeds, automated reporting, familiar to accountants

- Limitations: Requires manual trust accounting setup, no native tenant management

Real Estate-Specific Platforms:

- Buildium ($62/month flat rate, no minimum units): Native trust accounting, property-level tracking, automated owner reports, AI assistant

- AppFolio ($1.49/unit/month, 50-unit minimum): Smart bill entry, anomaly detection, built-in owner portal

Selection guidance: QuickBooks offers maximum accounting flexibility for smaller portfolios. Buildium provides the best value for 20-200 units with flat-rate pricing. AppFolio's automation suits 50+ unit portfolios despite higher cost.

Sources: AppFolio Pricing, Buildium Pricing

Step 4 - Establish a Consistent Recording Routine

Once your software is in place, the habits you build around it determine whether your records actually hold up. Uploading receipts, tagging expenses to specific properties, and reviewing transactions on a weekly or monthly basis prevents the year-end scramble.

Best practices:

- Create a cloud folder (Google Drive, Dropbox) for receipt storage

- Tag every transaction to a specific property immediately

- Review bank feeds weekly to catch errors early

- Schedule monthly reconciliation as a fixed calendar item task

Consistency matters more than perfection. Investors who review transactions monthly catch misclassified expenses and missing receipts while the details are still fresh, not six months later when a CPA is asking questions.

Step 5 - Consider Professional Support Early

Many investors underestimate bookkeeping complexity until they miss a major deduction, fail a lender audit, or face IRS scrutiny. Gross Consulting works directly with real estate investors to build bookkeeping systems structured for property-level tracking, lender reviews, and IRS compliance - from the first property onward.

Contact Gross Consulting:

- Phone: +1 (424) 347-6865

- Email: support@grossconsultinginc.com

- Hours: 8:00 AM - 7:00 PM MST

Key Tax Considerations and Deductions for Real Estate Investors

Common Deductible Expenses

IRS Publication 527 lists deductible rental property expenses:

- Mortgage interest (on loans used to acquire or improve the property)

- Property taxes

- Insurance premiums (property, liability, landlord policies)

- Repairs and maintenance (not improvements)

- Property management fees

- Professional services (legal, accounting, bookkeeping)

- Utilities paid by the owner

- Travel costs related to property management (the 2025 standard mileage rate is 70 cents per mile)

- Tax return preparation fees for Schedule E

Critical requirement: Every deduction requires documentation, and that documentation must be organized, not just saved.

Depreciation as a Strategic Deduction

Depreciation is one of the few tax benefits where you deduct a real cost without any cash leaving your pocket. The IRS lets you write off a portion of the building's cost each year, even as the property holds or grows in value, directly reducing taxable income.

Cost segregation studies take this further by reclassifying certain components (flooring, fixtures, landscaping) into shorter recovery periods, accelerating deductions for larger portfolios. Keep in mind:

- Bonus depreciation: 40% in 2025, declining to 0% by 2027

- Cost segregation: Still valuable after 2027 for reclassifying components, even without bonus depreciation

- Depreciation recapture: Tracked via your depreciation schedule from the acquisition date, critical for accurate bookkeeping at sale

Passive Activity Loss Rules and the $25,000 Allowance

Per IRS Publication 925, rental activities are passive even if you materially participate, unless you qualify as a real estate professional.

$25,000 special allowance:

- Available to active participants in rental real estate

- Phases out at 50% of modified AGI above $100,000

- Eliminated entirely at $150,000 MAGI

Active participation requirements:

- Making management decisions in a significant and bona fide sense (approving tenants, setting rental terms, approving expenditures)

- Minimum 10% ownership interest

Track active participation documentation and monitor AGI thresholds annually to preserve this deduction.

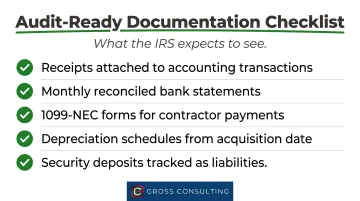

Audit Protection Through Clean Records

Unreconciled, incomplete, or improperly categorized books significantly increase audit risk and make it difficult to defend deductions if the IRS inquires.

Good documentation includes:

- Receipts attached to transactions in your accounting system

- Bank statements reconciled monthly

- Contractor payments properly reported via 1099-NEC forms

- Depreciation schedules maintained from acquisition

- Security deposits tracked as liabilities, not revenue

This habit pays for itself in risk reduction. The IRS announced in May 2024 its intention to increase audit rates for complex partnerships with assets over $10 million by nearly 10-fold to 1% by tax year 2026, signaling increased scrutiny on real estate structures.

Common Bookkeeping Mistakes Real Estate Investors Make

Treating a Separate Bank Account as a Complete Bookkeeping System

Many investors believe opening a property-specific bank account satisfies all bookkeeping requirements. That account alone fails to capture:

- Asset basis and depreciation schedules

- Loan principal vs. interest allocation

- Balance sheet items (security deposits, owner equity)

- Partner contributions and distributions

A bank account shows cash flow; bookkeeping captures the complete financial picture required for tax filing and lender reporting.

Ignoring the Balance Sheet and Focusing Only on the P&L

Most DIY investors track income and expenses but neglect the balance sheet entirely. This omission means:

- Cash may not reconcile due to missing escrow credits

- Loan principal and interest payments may be misclassified

- Security deposits may be incorrectly recognized as income

- Partner equity can be misreported

These errors create serious problems during tax prep, lender audits, or when seeking financing. The balance sheet is not optional. It's where asset basis, liability tracking, and equity structure actually live, and lenders know the difference.

These gaps compound over time, especially when investors delay building a proper system in the first place.

Delaying Setup and Assuming DIY Will Scale Indefinitely

The true cost of under-investing in bookkeeping is rarely visible until a stressful moment arrives:

- A lender requests up-to-date financials for refinancing

- Tax prep takes weeks longer than expected

- A missed deduction surfaces years later during an audit

Building a structured system early, whether through software or professional support, is far less expensive than the cleanup and rework required when the system breaks down. Investors managing three or more properties, juggling full-time work alongside investing, or struggling to produce clean financials on demand have likely already outgrown a DIY setup.

Frequently Asked Questions

Is QuickBooks good for real estate investors?

QuickBooks Online works well for most investors, especially for class tracking and automated bank feeds. Larger portfolios with active tenant management may benefit from real estate-specific platforms like AppFolio or Buildium, which offer native trust accounting and property-level reporting.

What expenses can you write off for investment property?

The main deductible categories include mortgage interest, property taxes, insurance, repairs and maintenance, depreciation, property management fees, professional services (legal and accounting), utilities, and travel related to property management. Note that capital improvements must be depreciated over time rather than deducted immediately.

What is the 50% rule in rental property?

The 50% rule is a quick estimation tool suggesting that approximately half of a rental property's gross income will go toward operating expenses (excluding mortgage payments). Investors use this rule of thumb to quickly screen whether a property is likely to generate positive cash flow before detailed analysis.

What is the difference between bookkeeping and accounting for real estate?

Bookkeeping covers the day-to-day work, recording and organizing every transaction. Accounting uses those records for analysis, reporting, tax strategy, and financial decision-making. Clean bookkeeping is required for any higher-level accounting work to be accurate.

Should I use cash or accrual accounting for my rental properties?

Cash basis is simpler and works well for most small to mid-sized portfolios. Accrual basis gives a more accurate picture and is often preferred by lenders or required for partnership-based portfolios, but most individual investors qualify for cash-basis accounting.

When should a real estate investor hire a professional bookkeeper?

Consider hiring a bookkeeper when you own three or more properties, can't generate clean financials on demand, or are preparing for a refinance or major transaction. At that point, professional support typically saves more in time, errors, and missed deductions than it costs.