Introduction

You spent years mastering legal theory, courtroom strategy, and client advocacy. But nowhere in law school did anyone teach you to manage trust accounts, reconcile ledgers, or build financial systems that keep your license safe and your firm profitable.

That gap has real consequences. Trust account violations remain among the most common reasons attorneys face bar discipline, according to The Florida Bar and ALPS Insurance. Cash flow problems derail promising practices. Compliance errors trigger audits. And attorneys lose an average of 5 hours daily to non-billable administrative work, including billing and bookkeeping, according to Clio's 2025 Legal Trends Report.

This guide covers the bookkeeping fundamentals every attorney needs to protect their practice and grow it:

- Setting up the right accounts from the start

- Managing trust funds in compliance with bar rules

- Tracking revenue and expenses accurately

- Deciding when to bring in professional help

Done right, law firm bookkeeping does more than satisfy the IRS - it protects your license, stabilizes your cash flow, and gives you a clear picture of where your firm actually stands.

TLDR: Key Takeaways

- Legal bookkeeping differs from standard bookkeeping, trust accounting rules, fiduciary duties, and state bar requirements all apply

- Every law firm needs separate operating and IOLTA/trust accounts; mixing those funds is an ethical violation that can cost you your license

- Pick your accounting method, cash or accrual, before filing your first return; it shapes how retainers and revenue are recorded

- Run three-way reconciliation on trust accounts every month, bank balance, ledger, and per-client balances all need to align

- Consistent, accurate bookkeeping protects your license, builds client confidence, and gives you the financial visibility to grow

Law Firm Bookkeeping vs. Accounting: Why the Distinction Matters

Bookkeeping is the daily recording, categorizing, and reconciling of transactions, the data layer everything else depends on. Accounting is the analytical layer: interpreting that data to produce financial statements, file taxes, and guide strategic decisions.

Both roles matter, and each has a distinct job in a law firm:

- Bookkeeper: logs trust deposits, categorizes expenses, and reconciles bank statements to create an accurate financial foundation

- Accountant: uses that clean data to calculate tax liability, identify profitable practice areas, and forecast cash flow

Attorneys reviewing their own books often try to handle both, and that's where the lines blur.

Many solo and small-firm attorneys collapse both functions into one, handling everything themselves. That approach causes errors, missed deductions, and compliance gaps. Research from Clio shows that 72% of firms unsatisfied with their revenue find general accounting "frustrating," compared to just 48% of satisfied firms, suggesting poor bookkeeping practices directly correlate with poor financial outcomes.

Setting Up Your Law Firm's Financial Foundation

Minimum Bank Account Structure

Every law firm needs at least two bank accounts:

- Operating/checking account for day-to-day revenue and expenses

- IOLTA or client trust account for client funds (retainers, settlement funds, advanced costs)

Optionally, add a savings account for tax reserves or planned expenditures. Open these accounts before accepting any client money, compliance and ethical practice depend on it.

Cash vs. Accrual Accounting Method

Choose your accounting method before filing your firm's first tax return. Changing it later is possible, but rarely simple.

Cash basis records income when received and expenses when paid. It's simpler, common for small firms, and delays tax on unearned income. IRS Publication 538 confirms Qualified Personal Service Corporations in the field of law may use the cash method. The Tax Cuts and Jobs Act expanded cash-method eligibility to businesses with average annual gross receipts of $25 million or less, covering most solo and small law firms.

Accrual basis records revenue when earned and expenses when incurred, providing a more accurate long-term view. Some jurisdictions require it for certain firm structures.

Most small law firms benefit from the cash method's simplicity and flexibility.

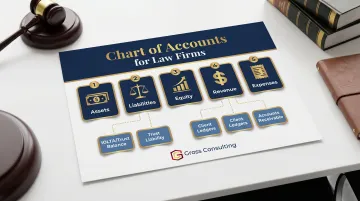

Chart of Accounts for Law Firms

Your chart of accounts organizes all financial transactions into five core categories:

- Assets (cash, accounts receivable, equipment)

- Liabilities (trust funds held, payables, loans)

- Equity (owner capital, retained earnings)

- Revenue (legal fees, settlements)

- Expenses (rent, salaries, insurance)

Law firms need additional sub-accounts:

- IOLTA/trust account balance

- Trust liability (money owed to clients)

- Client ledgers (individual balances)

- Accounts receivable (unpaid invoices)

Warning: Don't over-complicate the chart of accounts. Too many line items slow down reconciliation and increase error rates.

Basic Bookkeeping Infrastructure

Three systems need to be in place before your first client billing:

- Recordkeeping cadence - Enter transactions daily or batch them weekly at minimum. Waiting until year-end creates errors, compliance exposure, and poor visibility into cash flow.

- Invoicing process - Track billable hours as a direct input to revenue. Time-tracking and invoicing are linked, gaps here lead to money leakage.

- Financial workflows - Standardize how you record expenses, pay vendors, and withdraw earned fees from trust accounts.

Essential Financial Records

Maintain these records to stay compliant:

- Client ledgers

- Retainer agreements

- Trust account records

- Expense receipts

- Bank statements

- Tax-related documents

ABA Model Rule 1.15 requires "complete records" with a five-year minimum retention period after termination of representation. The IRS recommends seven years for tax records. The safest approach: retain records for seven years to satisfy both standards.

Trust Accounting and IOLTA: The Compliance Core

What is Trust Accounting and Why It Matters

Client funds, retainers, settlement funds, advanced costs, belong to the client until earned or disbursed. They cannot be used for firm expenses and must be held in a separate, designated account.

Mishandling trust funds ranks among the leading causes of attorney discipline, suspension and disbarment included, according to ALPS Insurance and The Florida Bar.

IOLTA Explained

IOLTA stands for Interest on Lawyers' Trust Accounts. When lawyers hold nominal or short-term client funds that can't earn net interest for the individual client, those funds are pooled into a single interest-bearing trust account. Interest earned is forwarded to state-administered legal aid programs, not to the firm or client.

IOLTA programs operate in all 50 states, the District of Columbia, Puerto Rico, and the U.S. Virgin Islands, generating over $4 billion since 1981, according to the ABA Commission on IOLTA. Rules and eligibility vary by state, verify your jurisdiction's specific requirements.

Commingling: A Critical Violation

Commingling means mixing firm funds with client funds in any account, even temporarily or accidentally, and it can trigger disciplinary action.

Practical safeguards:

- Never deposit operating funds into trust accounts

- Never pay firm expenses from trust accounts

- Keep detailed documentation of every trust transaction

- Maintain separation at all times

Three-Way Trust Reconciliation

Three-way reconciliation matches your trust bank statement, internal trust ledger, and individual client ledger balances. It's how you catch discrepancies before they become compliance problems, and most state bars require it at least monthly. Here's how to run it:

- Gather records (bank statement, trust ledger, client ledgers)

- Compare trust ledger to bank statement

- Confirm client ledger totals match trust ledger

- Document any timing differences

- Retain the reconciliation report

Common Trust Accounting Mistakes

Based on ALPS Insurance's analysis, the most damaging errors include:

- Recording retainer deposits as income - they're liabilities until earned

- Borrowing from client funds, even temporarily for payroll or taxes

- Applying one client's funds to a different matter

- Skipping monthly reconciliation, which lets errors compound

- Disbursing funds before deposited checks clear

- Withdrawing earned fees before the bill is delivered and reviewed

- Failing to maintain ledgers or document transactions

Consequences vary by jurisdiction. Consult your state bar for exact rules.

Essential Bookkeeping Best Practices for Law Firms

Establish a Consistent Recordkeeping Cadence

Procrastination is one of the most damaging bookkeeping mistakes. Waiting until year-end creates errors, compliance exposure, and an inability to make real-time financial decisions.

Minimum standards:

- Record transactions weekly

- Reconcile all accounts monthly

- Review financial reports monthly

Track Receivables and Invoice Promptly

Poor receivables management drains cash flow faster than most attorneys realize. Clio's 2025 Legal Trends Report shows firms collect 93% of invoiced amounts, but the compounding effect of realization (88%) and utilization (38%) means lawyers ultimately collect for only 2.4 hours of an 8-hour workday.

Key actions:

- Bill clients promptly after work is completed

- Set up a follow-up process for outstanding invoices

- Track aging receivables weekly

Use Financial Reports to Drive Decisions

Income statements, balance sheets, and cash flow statements aren't just for tax prep. Reviewed monthly, they answer the questions that drive real decisions:

- Which practice areas generate the most profit

- Where overhead can be trimmed without affecting output

- Whether the firm is on pace to hit annual revenue goals

Pair Technology with Professional Support

Firms using a hybrid approach, pairing legal-specific accounting software with professional bookkeeping support, reduce manual error risk and free attorneys to focus on billable work. That's where outside support pays off. Gross Consulting works with law firms and professional service businesses to build compliance-ready financial systems tailored to how attorneys actually operate. As a Verified Gusto Accountancy Partner, the firm handles payroll, operational bookkeeping, and the financial infrastructure firms need to scale.

Common Law Firm Bookkeeping Mistakes (and When to Call in Help)

The Most Consequential Mistakes

According to ALPS Insurance, these errors have compounding effects, the longer they go uncorrected, the harder the cleanup:

- Commingling operating and trust funds

- Recording IOLTA deposits as firm income

- Neglecting regular reconciliation

- Using general-purpose accounting software without trust accounting features

- Procrastinating on recordkeeping until year-end

Signs You Need Professional Bookkeeping Help

Any of these mistakes becoming routine is a signal worth taking seriously. Watch for these warning signs:

- Financial errors appear repeatedly with no clear cause

- Reconciliation is being skipped or delayed

- You're spending significant non-billable hours on bookkeeping

- Transaction volume has grown beyond what manual processes can handle reliably

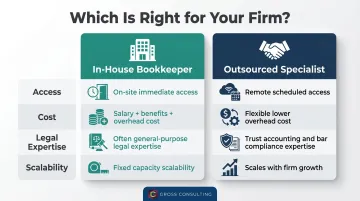

In-House vs. Outsourced Bookkeeper

Once you recognize the need for help, the next decision is where to find it. Here's how the two options compare:

| In-House Bookkeeper | Outsourced Specialist | |

|---|---|---|

| Access | On-site, immediate | Remote, scheduled |

| Cost | Salary + benefits + overhead | Flexible, lower overhead |

| Legal Expertise | Often general-purpose | Trust accounting and bar compliance |

| Scalability | Fixed capacity | Scales with firm growth |

What to Look for When Hiring or Outsourcing

- Experience with law firm trust accounting specifically

- Familiarity with legal billing workflows

- Knowledge of your jurisdiction's bar rules

- Compatibility with your accounting software

Bar complaints and disciplinary actions related to client funds are among the most serious consequences attorneys face, and many stem from bookkeeping errors that a general-practice accountant simply wasn't trained to catch. Vetting for legal-specific experience isn't optional; it's how you protect your license.

Frequently Asked Questions

What does a bookkeeper do at a law firm?

A law firm bookkeeper records daily transactions, manages operating and trust accounts, reconciles bank and trust ledgers, tracks retainers and client costs, and prepares financial records for the accountant or CPA.

Do law firms have bookkeepers?

Yes, many law firms use bookkeepers, either in-house or outsourced. Legal bookkeeping requires specific expertise in trust accounting and bar compliance rules that general bookkeepers may not have.

What are the legal requirements for bookkeeping?

ABA Model Rule 1.15 mandates separate client trust accounts, complete records, and a five-year minimum retention period after termination of representation. Specific rules vary by state bar jurisdiction. The IRS recommends seven-year retention for tax records.

What is the best accounting software for law firms?

Any software you choose must include trust accounting and IOLTA functionality, client/matter-level tracking, and reconciliation tools. Common choices reviewed by legal accounting experts include Clio Accounting, QuickBooks Online (with legal-specific add-ons), and Xero.

What is a reasonable charge for bookkeeping for a small company?

Rates vary by location, firm size, and service scope, and trust accounting expertise often pushes costs higher than standard bookkeeping. Monthly retainers are the most common pricing model. Contact Gross Consulting at (424) 347-6865 for a consultation.

What are the three golden rules of bookkeeping?

The three golden rules are: debit the receiver, credit the giver (personal accounts); debit what comes in, credit what goes out (real accounts); and debit all expenses and losses, credit all incomes and gains (nominal accounts). Applied consistently, these rules keep law firm ledgers accurate and audit-ready.